Overview of the year

During this financial year, 467 2022/23 audits were due to be completed under our contracts that cover 98% of eligible bodies. However, there is a large backlog of outstanding opinions. Only five 2022/23 audit opinions (1%) were given by the target date of 30 September 2023, adding to the backlog and the serious concerns about local public accountability and the impact on assurance about the sector’s governance and financial management.

Challenges in the local audit system

Since 2018 local government external audit has been affected by regulatory reforms, capacity issues and increased complexity, which has had a devastating impact on the delivery of audits and the backlog. This has had a profound effect on PSAA, impacting on many different areas of our appointing person role and increasing both the volume and complexity of our work.

The National Audit Office (NAO), the Public Accounts Committee (PAC) and the Levelling Up, Housing and Communities (LUHC) Select Committee have all highlighted the important challenges facing the local audit system and their serious consequences for accountability and effective management of the public bodies and services concerned.

In March 2023 the PAC considered the timeliness of local auditor reporting and published the outcome of its work in June 2023. Timeliness of local auditor reporting – Committees – UK Parliament. The report detailed the ongoing issues which are contributing to the deterioration. Delayed audits reduce accountability over £100 billion of local government spending and raise risks of financial issues going undetected. The report recommended that the Department of Levelling Up, Housing and Communities (DLUHC)[1] take action across a number of areas to address the deteriorating situation.

The LUHC Select Committee reported in November 2023 on the ongoing crisis in local audit and accountability. Financial Reporting and Audit in Local Authorities (parliament.uk). The report recognised the urgent action being taken by DLUHC to address the backlog but flagged up the need for longer-term solutions to prevent future backlogs. The report proposed five core purposes local authority accounts should serve to uphold local democracy and accountability.

[1] On 9 July 2024 DLUHC became the Ministry for Housing, Communities and Local Government (MHCLG)

Timeliness of audit completion

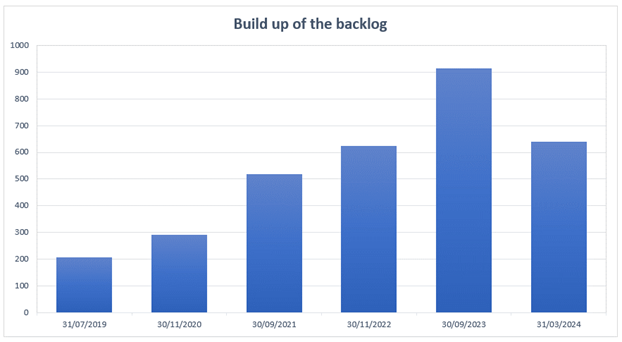

As at 31 March 2024 642 audits remained outstanding. Of these 164 related to 2022/23 and 478 to earlier years, meaning that only 119 (25%) audited bodies have up to date assurance on their financial position.

This position has built up incrementally year on year and has become pervasive. The table shows the number of outstanding audit opinions at each publishing date over the last five years, along with the position at 31 March 2024 which is half way through the current year.

The graph above illustrates that the number of audit opinions given in each of the last five years falls short of the circa 465 opinions due with the result that each annual shortfall is contributing to the total backlog.

As a result, too many bodies are making decisions, managing multiple financial challenges and laying plans for the future without the expected external audit assurance about their underlying financial positions.

Since the last publishing date of 30 September 2023 through to 30 June 2024 there have been 412 audit opinions given, and on 30 September 2024 the 464 2023/24 opinions become due.

Developments to address the issues

Following on from a number of Ministerial roundtables in Spring 2023, the Minister for Local Government published a cross-system statement in July 2023 setting out proposals to establish a series of backstop dates to tackle the audit backlog in England and embed timely audit Local Audit Delays – Cross-system statement on proposals to clear the backlog and embed timely audits.

The Statement included commitments from organisations involved in the regulation and oversight of local body financial reporting and audit (“system partners”). These system partners have been working collaboratively with the aim of designing a solution to clear the outstanding historical audit opinions and ensure that delays do not return.

PSAA has significant involvement in this process, proactively engaging with the local audit system to support the development of proposals to tackle the backlog along with fellow members of the Local Audit Liaison Committee. A number of groups were established to develop components of a proposed solution, and PSAA was a member of the Task and Finish Group and chaired the Handover Panel which considered the handover issues arising from the backlog. We are also a member of the workforce strategy steering group and the system risk register group.

In February 2024 a further cross-system Ministerial statement was published detailing the three stages (Reset, Recovery and Reform) of a proposed solution Local audit delays: Joint statement on update to proposals to clear the backlog and embed timely audit – GOV.UK (www.gov.uk).

The proposals were the subject of separate consultations led by DLUHC and NAO. A third consultation was launched by CIPFA on temporary changes to the Accounting Code of Practice. PSAA responded to the DLUHC and NAO consultations PSAA response to the DLUHC and NAO consultations to address the Local Audit Backlog in England.

The proposed solution requires sustained goodwill and commitment from all parties to remove the backlog, but it is critical to acknowledge that neither the reset nor the recovery phases address the fundamental and systemic problems in the supply market, or the capacity and recruitment/retention problems faced by finance teams in local bodies. These problems are acknowledged in the Joint Statement and will be a key focus of the reform phase when it is launched later this year.

At the time of writing the three consultations have concluded and we are expecting that these will provide a clearer sense of the reset and recovery plans, and a sense of the reform element later in the year. CIPFA has clarified that it is not going ahead with temporary changes and has moved its focus to longer term reform.

On 30 July the Government issued a statement setting out their intention to lay secondary legislation to provide for a series of backstop dates to clear the backlog over the next four years. This difficult but necessary solution has unprecedented consequences for the sector and the bodies affected, and recovery from it will be challenging for all parties. We look forward to the longer-term plans in the Autumn, and to playing our part in the welcome overhaul of the local audit system.

Audit services market

Our last main procurement took place in 2022 against a challenging backcloth of a troubled audit profession, a turbulent market and a local audit system facing unprecedented difficulties including large volumes of delayed audit opinions. Our procurement secured just enough audit supply for the bodies that opted into our scheme, but there was and remains little or no spare audit capacity. This is very concerning, as robust and timely audit is particularly vital in a period which is likely to continue to be challenging for local bodies.

Over the next few years, we anticipate that we will be required to make new auditor appointments when the new bodies created by the devolution agenda choose to opt into our scheme. We have used our dynamic purchasing system in 2023 to procure new auditor appointments, but with mixed success to date. This reflects the audit supply challenges, which are compounded by the uncertainty about how the audit backlog will be addressed and the resulting ask of auditors.

Commissioning and undertaking research to inform our work

We commission research each year on the impact on audit fees of changes in local audit requirements. It considers the likely fee implications of changes applicable under the Code of Audit Practice, including updated auditing and financial reporting standards. The research helps us to update scale fees and to review fee variation proposals. We publish the findings of the research to assist planning for local bodies and audit firms.

This year we commissioned independent consultants Touchstone Renard to perform a review of our work to develop the national auditor appointment scheme for the audits from 2023/24. The review concluded that PSAA had communicated and engaged effectively. Further details of the findings of the review are set out on page 13 of this annual report.

Setting audit fees and fee variations

PSAA’s work on fee scales and fee variations is driven by detailed requirements set out in regulations. There is a statutory deadline for us to set a fee scale, which is significantly in advance of the audit work. The early date combined with delayed audits and increasing audit requirements has added significant complexity to setting the fee scale, and also results in more fee variations. Ideally we would set the fee scale with full information on all audit requirements and following completion of the previous audits.

During 2023 PSAA consulted on and set the 2023/24 fee scale, the first of the new five-year appointing period. We updated all the scale fees to reflect the increased audit requirements. Our consultation set out the changes expected to have an impact on local audit work, and PSAA’s proposals for the additional fees needed. Our approach is to consolidate additional fees for ongoing requirements into the fee scale where we have sufficiently reliable information, for example from completed audits or from our externally provided technical research. Our proposals also included a substantial fee increase (151% on total fees) arising from our 2022 procurement, reflecting the very challenging market conditions).

Our consultation paper explained the difficulties in setting the fee scale at a time of significant change in the local audit system. While there was broad support for the fee scale proposals, particularly for the clarity it provided on audit fees, responses did also highlight concerns about the increase needed. We published the new fee scale on our website in November 2023.

Many of the issues raised by respondents extend beyond PSAA’s remit and relate to the need for radical change in the local audit system, and to achieve a more proportionate audit and a more sustainable audit system. We use this feedback when raising issues within the local audit system.

Monitoring our contracts and the quality of audit services

We published our fourth Annual Quality Monitoring Report (AQMR) that covered the work of local auditors appointed by us for the 2021/22 financial year. Our report aims to provide a rounded, well-informed view of performance and quality for each audit firm. The report included the outcome of the FRC’s inspections on the quality of local audit work. However, the audit backlog meant that the regulators inspected a much smaller sample of audit reviews than in previous years 10 rather than 37 – and only four of them were local government bodies. The FRC reported that the 10 financial statement audits and the nine value for money arrangements that they reviewed all met the required standard, as they judged them as either good or with only limited improvements required

Our AQMR also summarised our client survey of Audit Committee Chairs and Chief Finance Officers. The results reflected continuing challenges facing local audit with respondents expressing their concerns about the wider local audit regime. Recurring themes included the local impact of delayed audit opinions, the shortage of auditor resources, the level of fee variations, and the extent of the audit work now required on valuations of both property and pensions.

We have used the opportunity of moving to new contracts with audit firms to significantly evolve our monitoring and reporting arrangements. We have strengthened compliance requirements within the new contracts and have restructured ourselves to create additional capacity to deliver the new regime.

Proposals for local audit systems leadership

The Government commissioned Sir Tony Redmond to review local government financial reporting and audit, and our submission to him called for systems leadership. The Government proposed that a new regulator, the Audit, Reporting and Governance Authority (ARGA). will be the local audit system leader when it is created to replace the FRC. The FRC has created a Local Audit Unit in preparation, and in March 2023 the FRC and DLUHC published a memorandum of understanding outlining the FRC’s role and responsibilities in relation to the local audit system.

Since July 2021 DLUHC has acted as interim system leader, and established the Local Audit Liaison Committee (LALC). This committee enables closer working between system partners, with improved communications and coordination to work together to resolve the issues currently impacting local audit. We are on the LALC and are committed to playing an active role in addressing the challenges to move towards a local audit system which is more stable, resilient and sustainable.

Looking ahead

We will continue to monitor the local audit landscape and work hard to understand the potential implications of any change for opted-in bodies, audit firms, and key stakeholders. It is particularly important that the local audit market evolves, improving competition and assuring sustainability for the future.

The third appointing period will commence in April 2028. PSAA will need to secure audit services for opted-in bodies, so there is now a critical window to develop and strengthen the local audit system. The local audit market must improve to restore competition, and the system as a whole must explore all options to increase audit capacity and to ensure that audit work is proportionate and appropriate to the needs of the sector.

The current backlog solution proposals for first two phases of reset and recovery are a significant starting point on a long and crucially important journey. The third phase of reform is to address the systemic challenges that have led to the current local audit backlog. PSAA is ready to do everything we can as part of a collective systemwide effort to develop and deliver the critical changes required.

Board changes

On 31 March 2024 we said farewell to Steve Freer, a founding member and the Chair of PSAA’s Board. We are indebted to Steve for his outstanding contribution and dedication to PSAA’s work and development and to local audit over the last nine years.

We welcome our new Chair, Bill Butler who took up his appointment on 1 April 2024.

Bill Butler

Chair

Tony Crawley

Chief Executive